Regulation is the Answer to Reining in Algorithmic Stablecoins, but not in the Way Janet Yellen Thinks.

Regulation is the Answer to Reining in Algorithmic Stablecoins, but not in the Way Janet Yellen Thinks.

To preserve the benefits on blockchain-based digital dollars, policymakers need to pick winners.

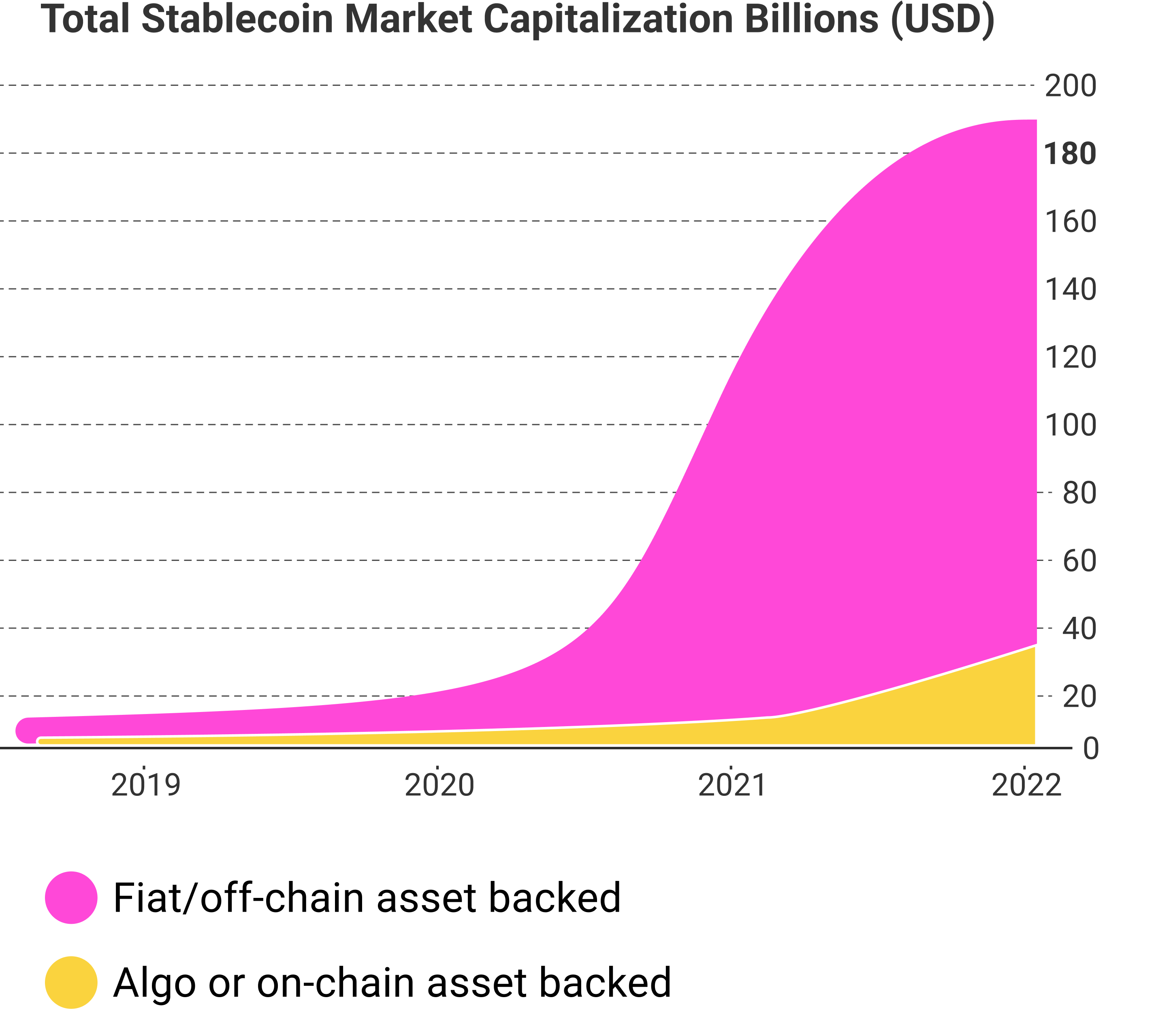

Since 2019, stablecoin supplies have grown 20x, now accounting for almost $200 billion or roughly 13% of the entire crypto market. This week, US Treasury Secretary Janet Yellen reiterated the need for stablecoin regulation by referencing the recent price slide of Terra USD (UST), the 3rd largest stablecoin and 11th largest cryptocurrency by market cap. Stablecoins are cryptocurrencies designed to maintain a value equal to $1. As relatively stable fiat-referenced assets, stablecoins improve upon existing cryptocurrencies as a medium of exchange, while still enjoying all the benefits of blockchain technology like programmability, transaction auditiability, and fast settlements.

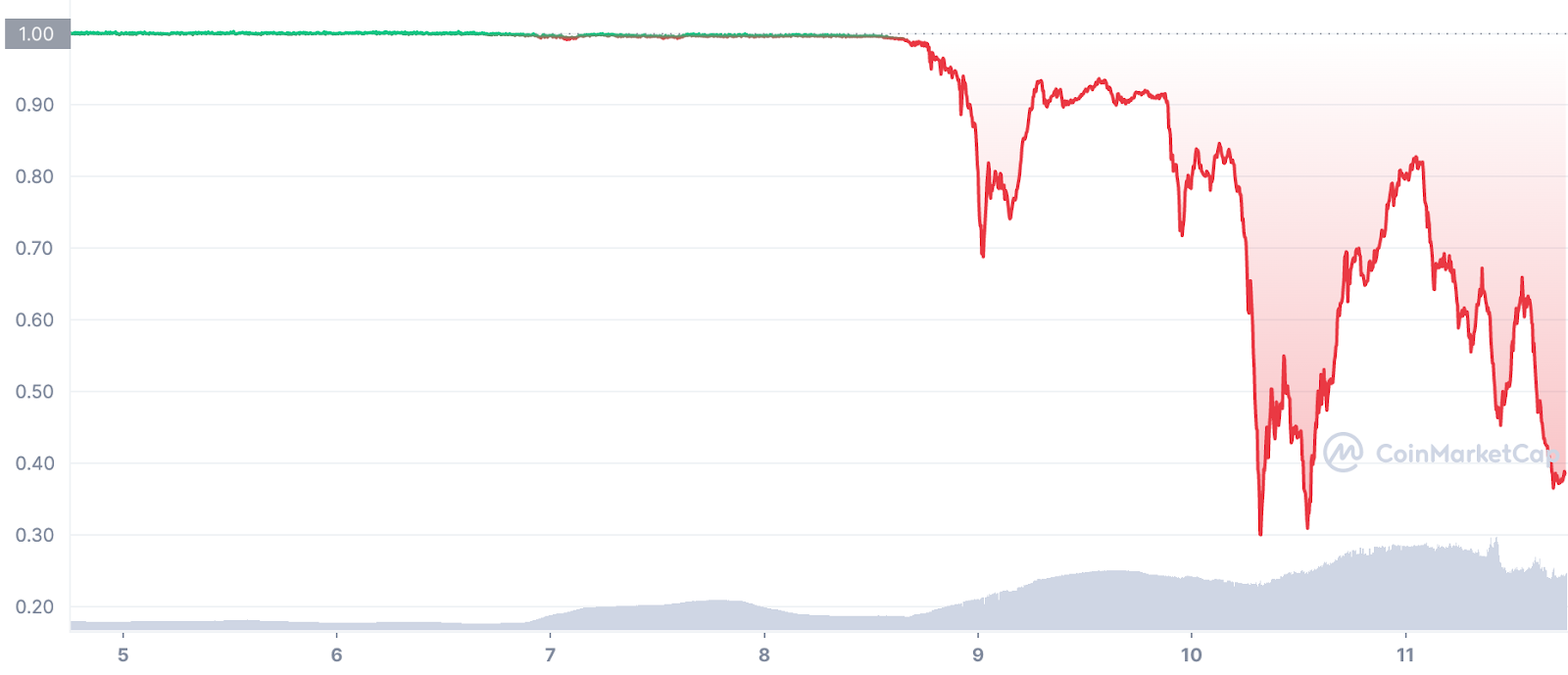

On May 9th, UST broke its target peg of $1, falling below $0.70 before plummeting below $0.30 today. Many in the space have predicted that this kind of event was possible, and the rest of us need only look to the recent history of stablecoins to see that not all stablecoins are created equal.

Why don’t we just ban stablecoins?

Unlike centralized stablecoins such as Circle’s USDC which uses collateral held in a custodial bank account to back their supply of tokens, algorithmic stabelcoins like UST use a mix of algorithms and adoption incentives to modify the supply of circulating coins in an effort to keep the price equal to $1. Because algorithmic stablecoins are governed by decentralized communities and autonomously executing smart contracts, no single entity is responsible for their stability. For this reason, algorithmic stablecoins are difficult to regulate.

The large-scale proliferation of algorithmic stablecoins could be disastrous for financial stability, but whether regulators like them or not, stablecoins are here to stay.

Centralized stablecoins have their problems too. If you’ve been in crypto for a minute, you’re familiar with Tether’s USDT, the accusations that it doesn’t have the reserves to cover its supply, and the associated fines levied on its parent company Bitfinex. At a market cap of $83 billion, USDT slipped to a trading price of $0.97 today - adding a new source of anxiety to an already panicked crypto market. Tether’s price slide is the result of uncertainty about whether or not Bitfinex will be able to pay out when token holders come knocking. Proper regulations that require issuer transparency could easily put such uncertainties to rest.

Regulators need to think carefully about how they use the political will motivated by recent events. An outright ban on stablecoins would not put an end to algorithmic stablecoins, and could make them a more dominant trading instrument within crypto markets while taking regulable actors out of the game entirely.

Algorithmic stablecoins account for less than $40 billion and have experienced extreme growth over the last 12 months with the decentralized finance boom. As the crypto markets ebb and flow through cycles of growth and decline, algorithmic stablecoins will follow them. If the last three crypto adoption cycles have demonstrated anything, it's the potential of an obscure digital asset to go from an afterthought to a cultural movement that inspires the public to reimagine its relationship with money - even if they have an incomplete understanding of the enabling technology.

The same forces that drove UST to the 11th largest cryptocurrency by market cap could easily drive other stablecoins with equally unreliable traits to large-scale adoption - incentivizing early adoption, and staying stable for long enough until its eventual failure brings down vastly more value with it. Had Luna’s Do Kwon achieved his vision, UST would be used to buy everything from diapers to securities and its failure would adversely affect the smooth functioning of our economies.

Political and macroeconomic forces could drive this kind of adoption as well. This scenario is difficult to imagine, but consider the political fervor and attitudes towards global financial elites in the wake of the 2008 financial crisis. If citizens had a subversive and high-quality alternative to the dollar, would they have used it? Circumstantial evidence suggests it's possible. Countries experiencing bouts of hyperinflation tend to be countries where US dollar-pegged stablecoins are more broadly accepted by merchants, and while this is largely done out of necessity to protect wealth, it is nonetheless subversive.

What Can we do?

Paradoxically, while decentralized stablecoins may pose the most significant long-term threat to financial stability, they deserve the least amount of policy resources.

Instead, policymakers should focus on crafting an approach that makes centrally issued stablecoins safe, useful, reliable, and ultimately superior to decentralized stablecoins.

In Canada, OSFI seems to be okay with Banks issuing stablecoins that are redeemable for bank deposits, and the Department of Finance is weighing up whether to include stablecoins in the new Retail Payment Activities Act (RPAA) - a move that would put stablecoins within the Bank of Canada’s remit. OSFI should review the risks associated with bank-issued stablecoins - namely the possibility that an issuing bank lends out the underlying assets. Because stablecoins can be redeemed in large quantities, banks may face run risks if investors try to cash out all at once.

The Department of Finance should absolutely include stablecoins in RPAA regulations. For stablecoins regulated under the RPAA, the Bank should follow its own advice for Payment Service Providers (PSPs) and require issuers to fully back their supply of coins in a custodial account or trust that pays out holders in the event of the issuer's insolvency.

As an additional step to curb Canada’s exposure to algorithmic stablecoins, Canadian securities regulators could use the same strong-arming techniques they’ve used to remove Tether’s USDT from Canadian Crypto exchanges, and even create informal guidelines that allow them to review new stablecoins on an ongoing basis.

With excellent options issued by Canadian banks and regulated PSPs, businesses, consumers, and institutional investors will have to choose between a class of stablecoin with poor guarantees or one that is backed by the guiding hand of the state. By lending legitimacy to centrally issued stablecoins and their issuers, regulators can signal to investors that a safe option exists - effectively snuffing decentralized stablecoins in their nascency. The big money will flow towards trust, and the value-creating network of merchants, transactors, and third-party developers will follow.

If policymakers can preserve Canada’s legacy as a modern economy with a highly trusted financial system, Canada could even promote the export of CAD-denominated centrally issued stablecoins to users all over the globe, bootstrapping adoption through the well-developed remittance networks of its citizens and their foreign counterparts.

Žižek on regulating the commons applies here: "What if the direction of this fight should not be to dream about the moment when decentralized collaborative networks take overt the entire field, but to find another organization and form of power external to the commons that will regulate its functioning?"